- 연속값 입력(continuous-valued inputs)을 받는 선형 함수(linear functions)라는 다른 가설 공간(hypothesis space) 사용

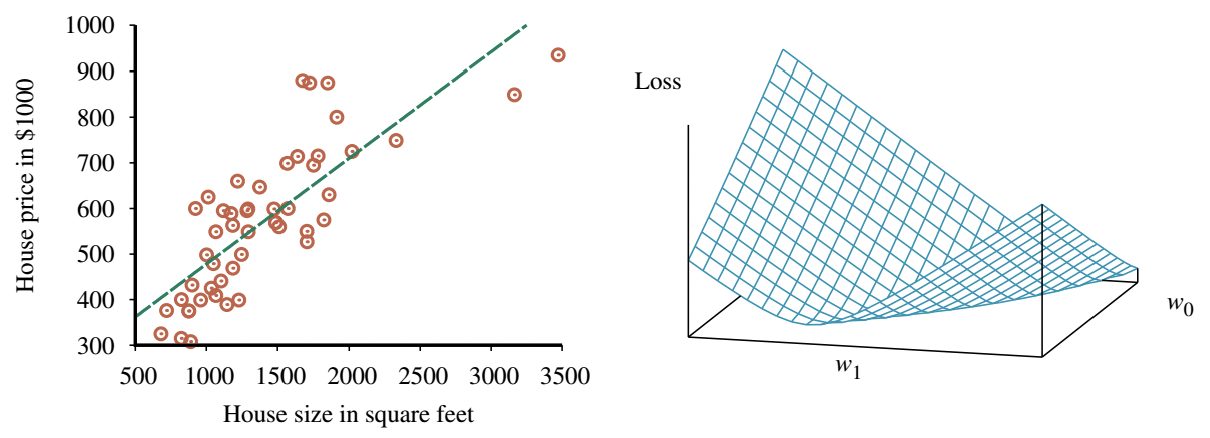

- Univariate linear function를 사용한 선형 회귀(linear regression), 즉 "직선 피팅(fitting a straight line)"을 다룸

- 다변수 사례(multivariate case) 및 경성/연성 임계값(hard and soft thresholds)을 적용하여 선형 함수를 분류기(classifiers)로 변환하는 방법도 포함

- 입력 x와 출력 y를 갖는 univariate 선형 함수(직선)의 형태

- y=w1x+w0

- w1과 w0는 학습할 실수 값의 계수(coefficients)

- 이 계수들을 가중치(weights)라고 부름.

- 항들의 상대적 가중치 변경으로 y 값 변화

- 가중치 벡터(vector) w를 <w1, w0>로 정의

- 가설(hypothesis) 함수: hw(x)=w1x+w0

- 선형 회귀(linear regression)의 작업: 데이터(data)에 가장 잘 맞는 hw를 찾는 것

- 목표: 경험적 손실(empirical loss)을 최소화하는 가중치 w1, w0 찾기

- 전통적으로 L2라 불리는 제곱 오차 손실(squared-error loss) 함수를 모든 학습 예제에 대해 합산하여 사용

Loss(hw)=j=1∑NL2(yj, hw(xj))

=j=1∑N(yj−hw(xj))2

=j=1∑N(yj−(w1xj+w0))2

- 목표: w∗=argminwLoss(hw) 찾기

- 손실 합 ∑j=1N(yj−(w1xj+w0))2은 w0와 w1에 대한 편도함수(partial derivatives)가 0일 때 최소화됨.

- 0으로 설정되는 방정식

∂w0∂j=1∑N(yj−(w1xj+w0))2=0

and

∂w1∂j=1∑N(yj−(w1xj+w0))2=0

- 이 방정식들은 유일해(unique solution)를 가짐

w1=N∑jxj2−(∑jxj)2N∑jxjyj−(∑jxj)(∑jyj)

w0=N∑jyj−w1(∑jxj)

∂w0∂j=1∑N(yj−(w1xj+w0))2=∂w0∂j=1∑N(w02−2(yj−w1xj)w0+…)

=j=1∑N(2w0−2(yj−w1xj))=0

∴Nw0=j=1∑Nyj−w1j=1∑Nxj

∴w0=N∑jyj−w1(∑jxj)

∂w1∂j=1∑N(yj−(w1xj+w0))2

=∂w1∂j=1∑N(xj2w12+2xj(w0−yj)w1+…)

=j=1∑N(2xj2w1+2xj(w0−yj))=0

∴j=1∑Nxj2w1+j=1∑N(xjw0−xjyj)=0

∴j=1∑Nxj2w1+j=1∑Nxj(N∑kyk−w1∑kxk)−j=1∑Nxjyj=0

- (슬라이드 표기 ∑k는 ∑j와 동일)

- 양변에 N을 곱하고 w1에 대해 정리

∴Nj=1∑Nxj2w1+(j=1∑Nxj)(j∑yj−w1j∑xj)−Nj=1∑Nxjyj=0

∴(Nj=1∑Nxj2−(j=1∑Nxj)(j∑xj))w1

=Nj=1∑Nxjyj−(j=1∑Nxj)(j∑yj)

∴w1=N∑jxj2−(∑jxj)2N∑jxjyj−(∑jxj)(∑jyj)

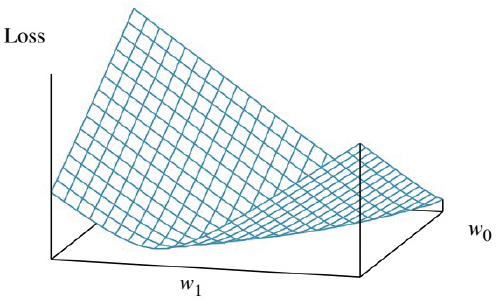

- 많은 학습 형태가 손실(loss)을 최소화하기 위해 가중치(weights)를 조정하는 것을 포함하며, 가중치 공간(weight space)에서 일어나는 일에 대한 시각적 이해가 도움됨.

- 가중치 공간: 가능한 모든 가중치 설정으로 정의되는 공간

- 예: Univariate 선형 회귀의 경우, w0와 w1로 정의되는 가중치 공간은 2차원

- 손실 함수(loss function)를 w0와 w1의 함수로 3D plot에 시각화 가능

- 손실 함수는 볼록(convex) 함수이며, 이는 L2 손실 함수를 사용하는 모든 선형 회귀 문제에서 사실임

- 볼록 함수는 지역 최적해(local optima)가 아닌 전역 최적해(global optimum)를 보장

- Univariate linear model은 편도함수가 0이 되는 최적의 해를 찾기 쉽다는 좋은 특성을 가짐

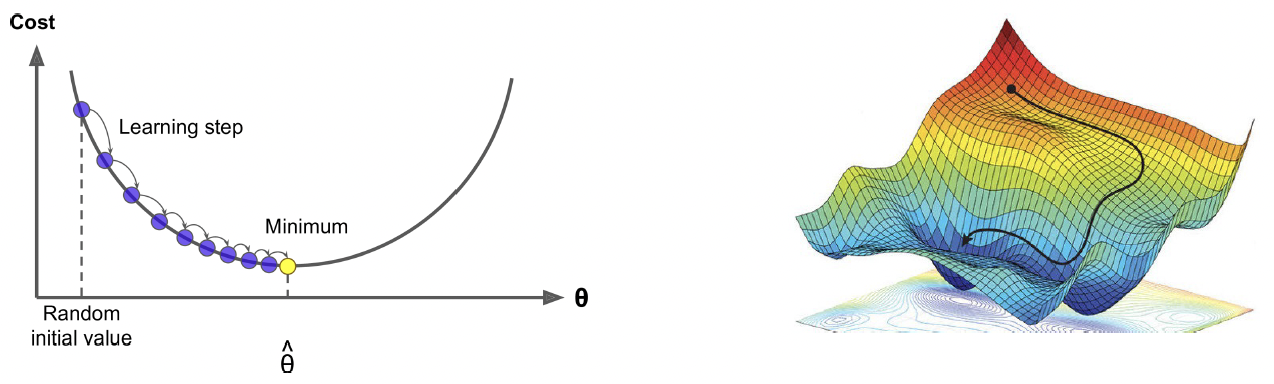

- 하지만 항상 분석적인 해를 구하기 쉬운 것은 아니므로, 도함수의 0 지점을 찾는 해법에 의존하지 않고 복잡성에 상관없이 모든 손실 함수에 적용 가능한 손실 최소화 방법을 도입

- 연속적인 가중치 공간(continuous weight space)을 매개변수의 점진적 수정을 통해 탐색: 경사 하강법(Gradient Descent)

- 가중치 공간에서 임의의 시작점(starting point) 선택

- 예: 선형 회귀의 (w0, w1) 평면

- 경사(gradient)의 추정치 계산

- 가장 가파른 내리막 방향(steepest downhill direction)으로 약간 이동

- (local) 최소 손실을 갖는 가중치 공간의 한 지점으로 convergence할 때까지 반복

- 알고리즘

w← (매개변수 공간의 임의의 지점)

while (수렴되지 않는 동안) do

for (w의 각 wj에 대해) do

wj←wj−α∂wj∂Loss(w)

- 매개변수 α는 learning rate(학습률) 또는 step size(스텝 크기)라고 불림

- α는 고정 상수(fixed constant)일 수도 있고, 학습 과정이 진행됨에 따라 시간 경과에 따라 감소(decay)할 수도 있음.

- 단변량 회귀의 경우, 손실은 이차(quadratic)식이므로 편도함수는 선형(linear)이 됨.

- 하나의 훈련 예제 (x, y)만 있는 단순화된 경우

∂wi∂Loss(w)=∂wi∂(y−hw(x))2

=2(y−hw(x))⋅∂wi∂(y−hw(x))

=2(y−hw(x))⋅∂wi∂(y−(w1x+w0))

- w0와 w1 모두에 적용

∂w0∂Loss(w)=−2(y−hw(x))

∂w1∂Loss(w)=−2(y−hw(x))⋅x

- 이 결과를 원래의 경사 하강법 방정식에 대입하고, 2를 명시되지 않은 학습률 α에 포함시키면, 다음 학습 규칙(learning rule)을 얻음

w0←w0+α(y−hw(x))

w1←w1+α(y−hw(x))⋅x

- 이 업데이트는 직관적으로 이해 가능: 만약 hw(x)>y (즉, 출력이 너무 큼)이면, w0를 약간 줄이고, x가 양의 입력이면 w1을 줄이고 x가 음의 입력이면 w1을 늘림

- N개의 훈련 예제에 대해, 각 예제의 개별 손실 합계를 최소화하고자 함.

- 합의 도함수는 도함수의 합이므로

w0←w0+αj=1∑N(yj−hw(xj))

w1←w1+αj=1∑N(yj−hw(xj))⋅xj

- 이 업데이트는 단변량 선형 회귀를 위한 배치 경사 하강법(batch gradient descent) 학습 규칙 (결정론적 경사 하강법(deterministic gradient descent)이라고도 함)

- 모든 훈련 예제를 다루는 한 단계를 에포크(epoch)라고 함.

- 더 빠른 변형: 확률적 경사 하강법(stochastic gradient descent) 또는 SGD

- 각 단계에서 무작위로 적은 수의 훈련 예제를 선택하고, 경사 하강법 방정식에 따라 업데이트

- 원래 SGD 버전은 각 단계마다 단 하나의 훈련 예제만 선택했지만, 현재는 N개 예제 중 m개의 미니배치(minibatch)를 선택하는 것이 더 일반적

- 일부 CPU 또는 GPU 아키텍처에서는, m을 선택하여 병렬 벡터 연산(parallel vector operations)을 활용, m개 예제로 스텝을 밟는 것이 단일 예제 스텝만큼 빠름.

- 이러한 제약 내에서, m을 각 학습 문제에 맞게 조정(tuned)해야 하는 하이퍼파라미터(hyperparameter)로 취급

- 미니배치 SGD의 수렴이 엄격하게 보장되지는 않음. 최소값 주변에서 안정되지 않고 진동(oscillate)할 수 있음.

- 이를 완화하기 위해 학습률 α를 감소시키는 스케줄(schedule)을 만들 수 있음.

- SGD는 선형 회귀 이외의 모델, 특히 신경망(neural networks)에 널리 적용됨.

- 손실 표면(loss surface)이 볼록하지 않은 경우에도, 이 접근 방식은 전역 최소값에 가까운 좋은 지역 최소값을 찾는 데 효과적임이 입증됨.

- 각 예제 xj가 n-요소 벡터인 multivariable linear regression(다변량 선형 회귀) 문제로 쉽게 확장 가능

- 가설 공간(hypothesis space)은 다음 형태의 함수 집합

hw(xj)

=w0+w1xj,1+w2xj,2+⋯+wnxj,n

=w0+i=1∑nwixj,i

- 더 간단한 표기를 위해, 항상 1과 같은 값을 갖는 가상의(dummy) 입력 속성 xj,0를 만듦.

- 그러면, h는 가중치와 입력 벡터의 dot product

hw(xj)=w⋅xj=wTx=i=0∑nwixj,i

- 최적의 가중치 벡터 w∗는 예제에 대한 제곱 오차 손실을 최소화 w∗=argminw∑jL2(yj, w⋅xj)

- 단변량 선형 회귀의 경우처럼, 경사 하강법은 손실 함수의 (유일한) 최소값에 도달

- 각 가중치 wi에 대한 업데이트 방정식

wi←wi+αj∑(yj−hw(xj))⋅xj,i

- 선형 대수(linear algebra)와 벡터 미적분(vector calculus)의 도구를 사용하면, 손실을 최소화하는 w를 해석적(analytically)으로 풀 수도 있음.

- y를 훈련 예제의 출력 벡터, X를 데이터 행렬(data matrix) (즉, 행당 하나의 n-차원 예제를 갖는 입력 행렬)이라 함.

- 예측된 출력 벡터는 y^=Xw

- 모든 훈련 데이터에 대한 제곱 오차 손실

L(w)=∣∣y^−y∣∣22=∣∣Xw−y∣∣22

∇WL(w)=∇W∣∣Xw−y∣∣22

=∇W(Xw−y)T(Xw−y)

=∇W[wTXTXw−2yTXw+yTy]

=2XTXw−2XTy

=2XT(Xw−y)=0

- 재정리하면, 최소 손실 가중치 벡터는 다음과 같음. (정규 방정식(Normal Equation)) w∗=(XTX)−1XTy

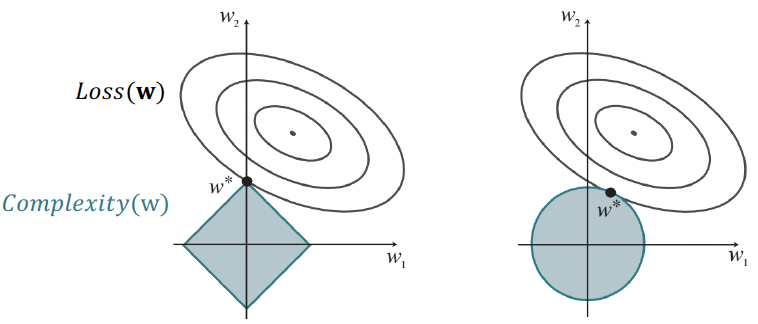

- 고차원 공간의 multivariable linear regression에서는 실제로는 관련 없는 차원이 우연히 유용한 것처럼 보여 과적합(overfitting)을 초래할 수 있음.

- 따라서, 과적합을 피하기 위해 다변량 선형 함수에 정규화(regularization)를 사용하는 것이 일반적

- 정규화를 사용하면 가설(hypothesis)의 총 비용(cost)을 최소화, 경험적 손실과 가설의 복잡도(complexity)를 모두 계산

Cost(h)=EmpLoss(h)+λ Complexity(h)

- 복잡도는 가중치의 함수로 지정 가능

Complexity(hw)=Lq(w)=i∑∣wi∣q

- q=1이면, L1 정규화, 절댓값의 합을 최소화

- q=2이면, L2 정규화, 제곱의 합을 최소화

- L1 정규화는 중요한 이점이 있음.

- 즉, 종종 많은 가중치를 0으로 설정하여, 해당하는 속성(attributes)이 완전히 관련 없다고 선언

- Loss(w)+λComplexity(w)를 최소화하는 것은 Complexity(w)≤c 제약 하에 Loss(w)를 최소화하는 것과 동일

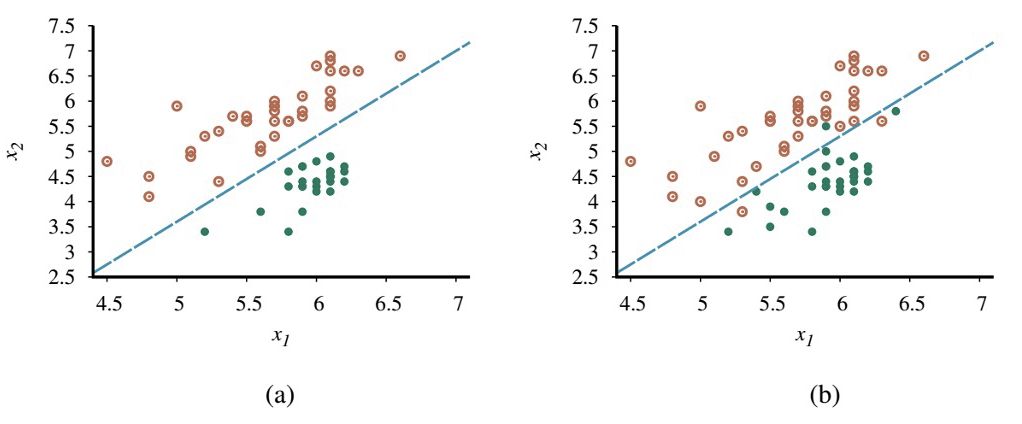

- 선형 함수는 regression뿐만 아니라 classification(분류)를 수행하는 데에도 사용 가능

- 결정 경계(decision boundary)는 두 클래스(classes)를 분리하는 선 (or 고차원에서는 표면)

- 선형 결정 경계는 linear separator라고 하며, 이러한 seperator를 허용하는 데이터를 linearly separable하다고 함.

−4.9+1.7x1−x2=0

w=[−4.9, 1.7, −1]

hw(x)=1 if w⋅x≥0 and 0 otherwise.

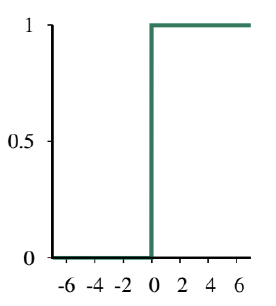

- h는 선형 함수 w⋅x를 임계 함수(threshold function)에 통과시킨 결과로 생각할 수 있음.

hw(x)=Threshold(w⋅x) where Threshold(z)

=1 if z≥0 and 0 otherwise.

- 문제: (1) 경사 하강법과 (2) 최적 가중치(w∗)를 도출하기 위한 닫힌 형태(closed form)의 계산, 둘 다 활용 불가

- w⋅x=0인 지점을 제외한 가중치 공간 거의 모든 곳에서 기울기가 0이고, w⋅x=0인 지점에서는 기울기가 정의되지 않기 때문

- 선형 함수의 출력을 임계 함수에 통과시키는 것이 선형 분류기(linear classifier)를 생성함을 확인

- 하지만 임계값의 경성(hard nature)은 몇 가지 문제를 야기

- 가설 hw(x)는 미분 불가능하며 입력과 가중치에 대해 불연속 함수임. 이는 perceptron rule을 사용한 학습을 매우 예측 불가능하게 만듦.

- 또한, 선형 분류기는 경계에 매우 가까운 예제에 대해서도 항상 1 또는 0의 완전한 확신에 찬 예측을 알림. 일부 예제는 명확한 0 또는 1로, 다른 예제는 불분명한 경계선 케이스로 분류할 수 있다면 더 좋을 것

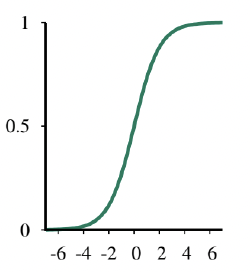

- 이 모든 문제는 임계 함수를 부드럽게(softening) 함으로써 (경성 임계값을 연속적이고 미분 가능한 함수로 근사) 크게 해결 가능

hw(x)=Logistic(w⋅x)

=1+e−w⋅x1

- Data set에 대한 손실을 최소화하기 위해 이 모델의 가중치를 맞추는(fitting) 과정: 로지스틱 회귀(logistic regression)

- 가설이 더 이상 0 또는 1만 출력하지 않으므로 L2 손실 함수 사용

- g를 로지스틱 함수, g′을 그 도함수로 사용

- 단일 예제 (x, y)에 대해, 기울기 유도는 h의 실제 형태가 삽입되는 지점까지 선형 회귀와 동일

∂wi∂Loss(w)=∂wi∂(y−hw(x))2

=2(y−hw(x))⋅∂wi∂(y−hw(x))

=−2(y−hw(x))⋅g′(w⋅x)⋅∂wi∂(w⋅x)

=−2(y−hw(x))⋅g′(w⋅x)⋅xi

- 로지스틱 함수의 도함수 g′은 g′(z)=g(z)(1−g(z))를 만족

∂z∂1+e−z1=∂z∂(1+e−z)−1

=−1⋅(1+e−z)−2⋅(−e−z)

=(1+e−z)2e−z

=1+e−z1⋅1+e−ze−z=g(z)(1−g(z))

따라서,

g′(w⋅x)=g(w⋅x)(1−g(w⋅x))

=hw(x)(1−hw(x))